What Is a Tokenized Fund?

Key Takeaways

- Tokenized funds are investment funds whose ownership shares are represented as digital tokens on a blockchain, enabling programmable ownership, improved settlement, and more efficient fund operations.

- Tokenization modernizes fund infrastructure, upgrading how ownership, settlement, and administration function while remaining compatible with existing regulatory frameworks and operational processes.

- Both public and private investment vehicles can adopt tokenization, spanning use cases from money market funds and ETFs to private credit, real estate, and alternative funds, often through hybrid models that combine onchain ownership with offchain operations.

- Chainlink provides the execution layer required for tokenized funds to operate at institutional scale, delivering trusted onchain data, secure cross-chain interoperability, atomic settlement workflows, embedded compliance logic, and seamless integration with existing financial systems.

Over the past decade, blockchain technology has evolved from providing alternatives to traditional financial systems into establishing core primitives increasingly used to improve them. Today’s blockchain infrastructure supports real-world use cases at scale across payments, settlement, identity, and asset issuance. As these systems have matured, the question is no longer whether blockchain belongs in traditional finance, but where and how it can deliver clear, functional advantages.

Tokenized funds are a leading use case driving this shift.

Despite the overwhelming prevalence of investment funds—approximately $147 trillion in global assets under management as of mid-2025—the infrastructure supporting fund ownership, settlement, and administration has changed little over time. Tokenization modernizes how fund interests are issued, managed, and accessed, optimizing how funds operate while preserving their underlying purpose.

How Tokenized Funds Work

At its core, fund tokenization involves representing ownership as digital tokens on a blockchain.

In a conventional fund, investor ownership is recorded and maintained through centralized systems. Subscriptions, redemptions, and ownership updates typically rely on batch processes, reconciliation across multiple intermediaries, and delayed settlement cycles—introducing friction for both issuers and investors.

A tokenized fund preserves the economic structure of a traditional fund but changes how ownership is represented and managed. Tokenizing and bringing fund ownership onchain enables faster settlement, greater transparency, and more automated fund operations. These capabilities form the foundation for new efficiencies and distribution models, enhancing utility for both institutional and retail participants.

Benefits of Tokenized Funds

Tokenization unlocks a range of practical benefits that improve how funds operate, distribute, and scale.

Liquidity & Composability

Tokenized funds support 24/7 transferability on blockchain networks, enabling continuous access and faster movement of capital. While regulatory and fund-specific rules still apply, tokenization makes it technically possible for fund interests to be transferred or settled at any time, improving liquidity and flexibility for investors.

Beyond simple transferability, tokenization also enables composability—the ability for fund interests to be programmatically integrated with other onchain financial systems, including decentralized finance (DeFi) applications where permitted. Tokenized fund shares can be used in additional contexts, such as serving as collateral within lending protocols, participating in liquidity frameworks, or supporting structured yield strategies. This extends the utility of fund ownership beyond traditional buy-and-hold models, unlocking new forms of capital efficiency while preserving the fund’s underlying structure.

Improved Operational Efficiency

Tokenization introduces automation across the fund lifecycle. Smart contracts streamline processes such as subscriptions, redemptions, recordkeeping, and corporate actions, reducing reliance on manual workflows and intermediary coordination. By minimizing reconciliation and shortening execution timelines, tokenized funds lower administrative costs and improve operational resilience for fund managers and service providers.

Fractional Ownership and Broader Access

Because digital tokens are inherently divisible, tokenized funds support fractional ownership more naturally than traditional fund structures. This lowers minimum investment thresholds and enables broader access, particularly in asset classes such as real estate, private credit, and private equity that have historically been difficult for smaller investors to access.

Enhanced Transparency and Auditability

Tokenized funds leverage blockchain-based recordkeeping, where ownership changes and transactions are recorded on a tamper-resistant ledger that is independently verified in real time. This creates a shared, authoritative view of fund ownership, improving auditability and reducing information asymmetries across issuers, investors, and service providers.

Types of Tokenized Funds

Tokenized funds can broadly be grouped into public and private categories. While both use blockchain-based tokens to represent ownership, they differ in structure, accessibility, and regulatory treatment.

Tokenized Public Funds

Tokenized public funds mirror traditional publicly offered investment vehicles, such as mutual funds, exchange-traded funds (ETFs), and money market funds. These funds are typically subject to established regulatory frameworks and are designed for broad investor participation, with eligibility requirements varying by jurisdiction.

Common examples include tokenized money market funds that invest in short-term, high-quality debt instruments such as U.S. Treasuries; tokenized mutual funds that preserve traditional portfolio mandates and governance structures; and tokenized ETFs that replicate exchange-traded products while benefiting from blockchain-based settlement and recordkeeping.

In these models, tokenization primarily enhances operational efficiency, transparency, and distribution, while the underlying investment strategy and regulatory oversight remain largely unchanged.

Tokenized Private Funds

Tokenized private funds represent ownership in private investment vehicles such as hedge funds, private credit funds, venture capital funds, or real estate funds. Historically, these funds have been limited to accredited or institutional investors due to regulatory and liquidity constraints.

Tokenization can improve efficiency and access for private funds by enabling fractional ownership of traditionally illiquid assets, streamlining fund administration and reporting, and supporting more flexible transfer and settlement mechanisms—subject to compliance requirements.

Examples include tokenized private credit funds, real estate funds, and alternative investment vehicles that leverage blockchain infrastructure while maintaining controlled access through investor eligibility checks.

Hybrid Models

Some tokenized funds adopt hybrid models, where the fund operates within existing offchain structures while issuing onchain representations of fund interests. This approach allows asset managers to adopt tokenization incrementally—enhancing distribution, settlement, and transparency—while remaining aligned with existing regulatory frameworks and operational processes.

While fully onchain funds remain an emerging area due to regulatory and market considerations, they illustrate the broader direction of fund tokenization as infrastructure, standards, and compliance frameworks continue to mature.

How Chainlink Enables Tokenized Funds at Scale

Tokenized funds modernize how ownership, settlement, and administration function—but delivering these benefits at an institutional scale requires more than token issuance alone. Funds must operate with reliable valuation data, settlement guarantees, cross-chain interoperability, embedded compliance, and native integration with existing financial infrastructure.

At institutional scale, the success of tokenized funds depends on how effectively they integrate with the systems asset managers, administrators, and custodians already rely on.

Chainlink provides this foundational infrastructure, enabling tokenized funds to meet the security and reliability standards required for global capital markets.

Bringing Fund Operations Onchain

One of the most immediate challenges in fund tokenization is operational continuity. Asset managers and administrators cannot abandon existing systems overnight, nor can they fragment workflows across disconnected environments.

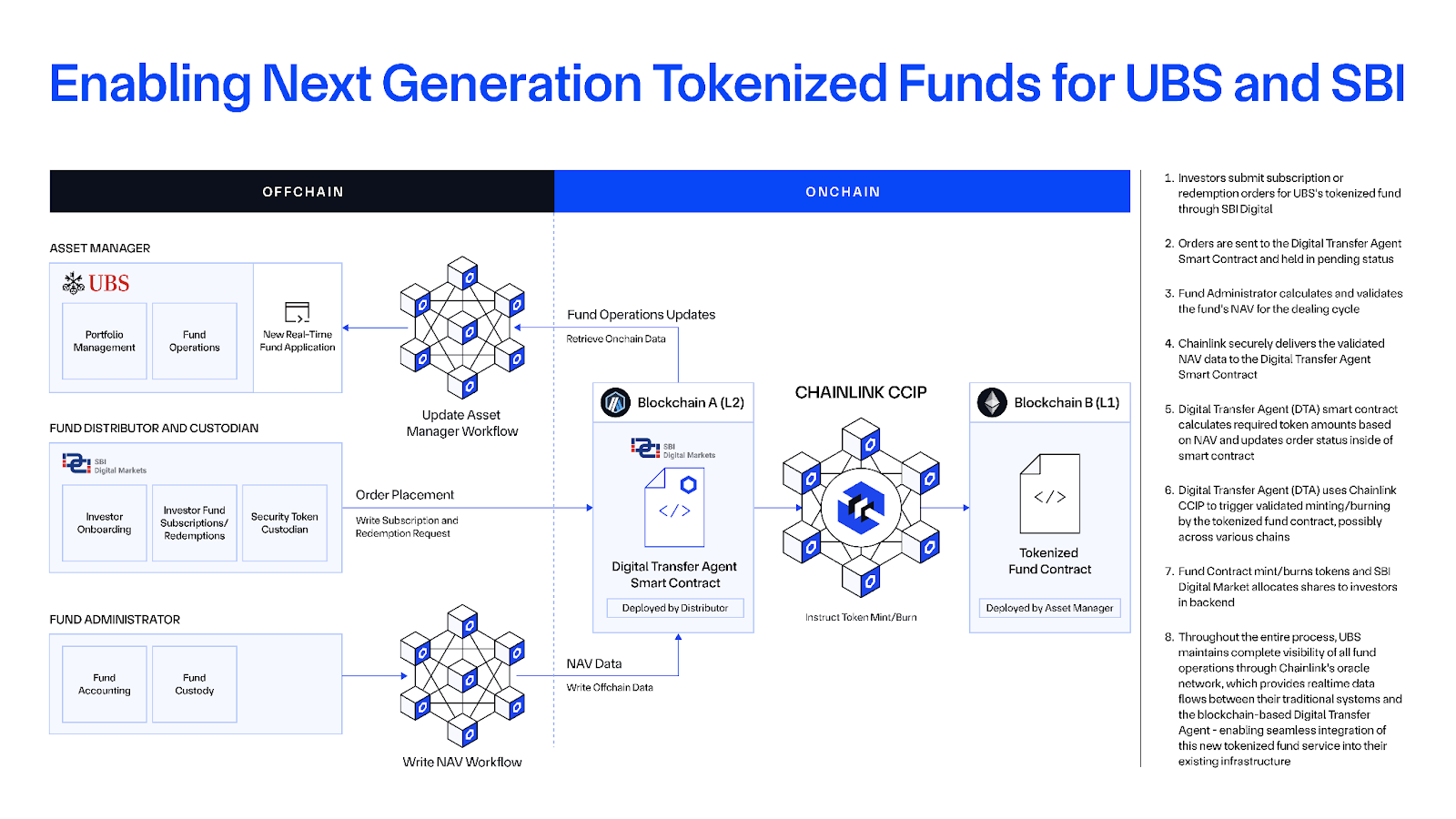

As part of the Monetary Authority of Singapore’s Project Guardian, institutions including UBS Asset Management, SBI Digital Markets, and Chainlink demonstrated how tokenized funds can operate with onchain share registers while continuing to integrate with existing operational processes. In this model, fund ownership is maintained onchain, while lifecycle workflows, such as subscriptions and redemptions, are orchestrated through Chainlink’s Cross-Chain Interoperability Protocol (CCIP).

This approach allows funds to adopt tokenization incrementally, enhancing settlement efficiency, transparency, and automation without disrupting established regulatory or administrative frameworks.

Reliable Onchain NAV and Pricing

Accurate and timely valuation is foundational to fund operations, particularly for money market and liquidity funds, where price stability is critical. Traditional fund infrastructure often limits NAV updates to end-of-day calculations, constraining intraday liquidity and secondary market activity.

Chainlink enables NAV and pricing data to be delivered onchain in a secure, automated, and cryptographically verifiable manner. An initiative between Sygnum Bank, Fidelity International, and Chainlink demonstrated how real-time NAV data can be published onchain for Fidelity’s Institutional Liquidity Fund.

By making NAV data directly available to smart contracts, tokenized funds can support more efficient pricing, settlement, and automated servicing—unlocking liquidity while maintaining pricing integrity.

Delivery versus Payment (DvP) Synchronization

Settlement remains one of the most complex and risk-prone aspects of fund operations. Traditional funds rely on extended settlement cycles, with asset and cash movements occurring across separate financial systems, introducing reconciliation overhead and settlement risk.

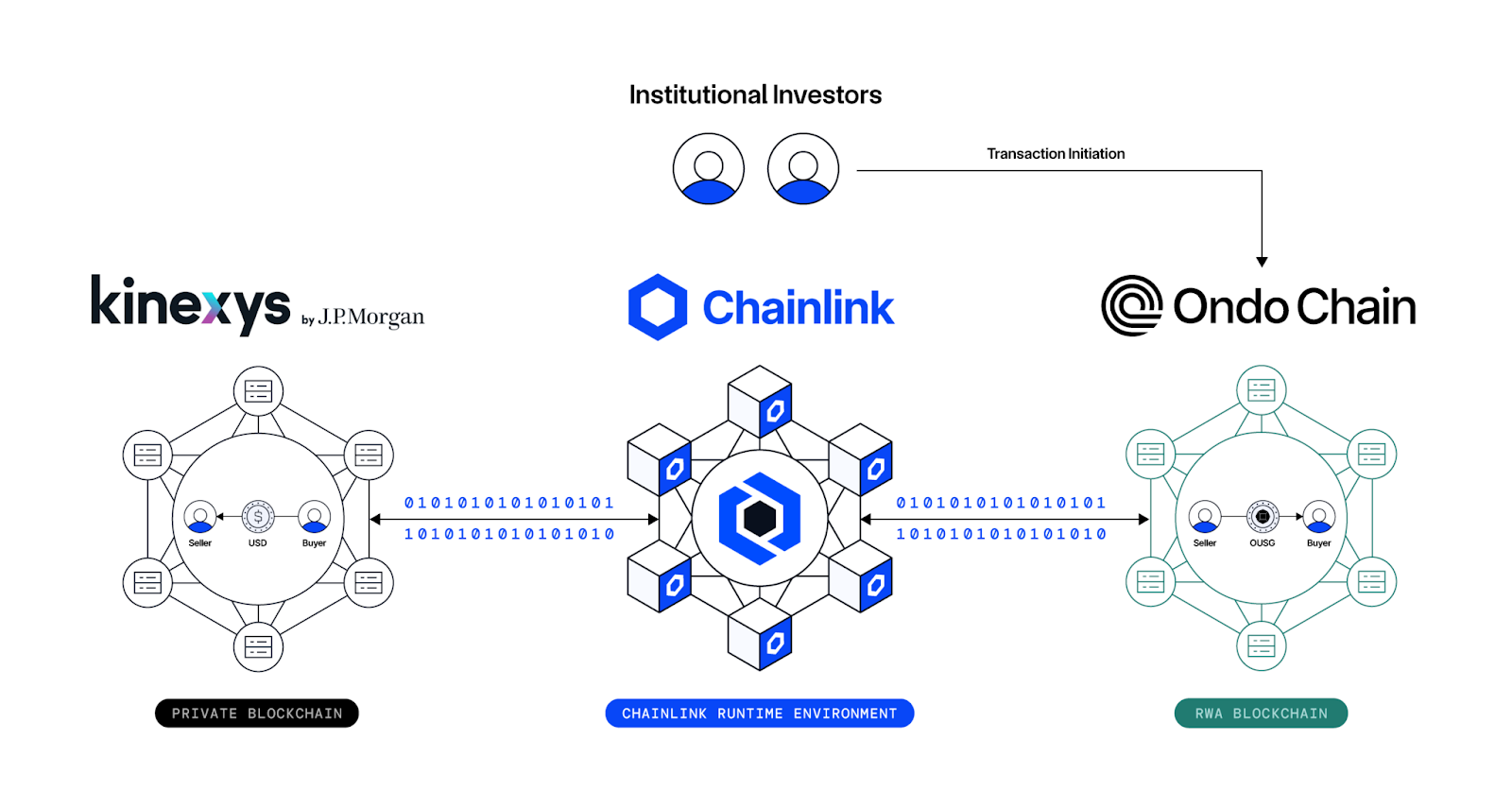

Chainlink infrastructure enables the transition toward atomic DvP workflows by securely coordinating asset and payment legs across traditional and blockchain-based systems. A recent initiative between Kinexys by J.P. Morgan, Ondo Finance, and Chainlink demonstrated this model by executing an atomic DvP transaction involving tokenized U.S. Treasury fund units and digital payment tokens.

As digital cash infrastructure continues to evolve, these workflows immediately illustrate how tokenized funds can reduce settlement risk and operational complexity.

Embedded Compliance, Verifiable Identity, and Privacy

Tokenized funds must operate within strict regulatory requirements, including investor eligibility, jurisdictional restrictions, and transaction controls. Managing these constraints purely offchain reintroduces friction and limits overall efficiency.

Chainlink enables compliance logic to be embedded directly into onchain workflows through its compliance and identity frameworks, including the Automated Compliance Engine (ACE) and Cross-Chain Identity (CCID). These solutions allow verified credentials,such as KYC status or investor classification, to be represented onchain as cryptographic proofs without exposing sensitive personal data.

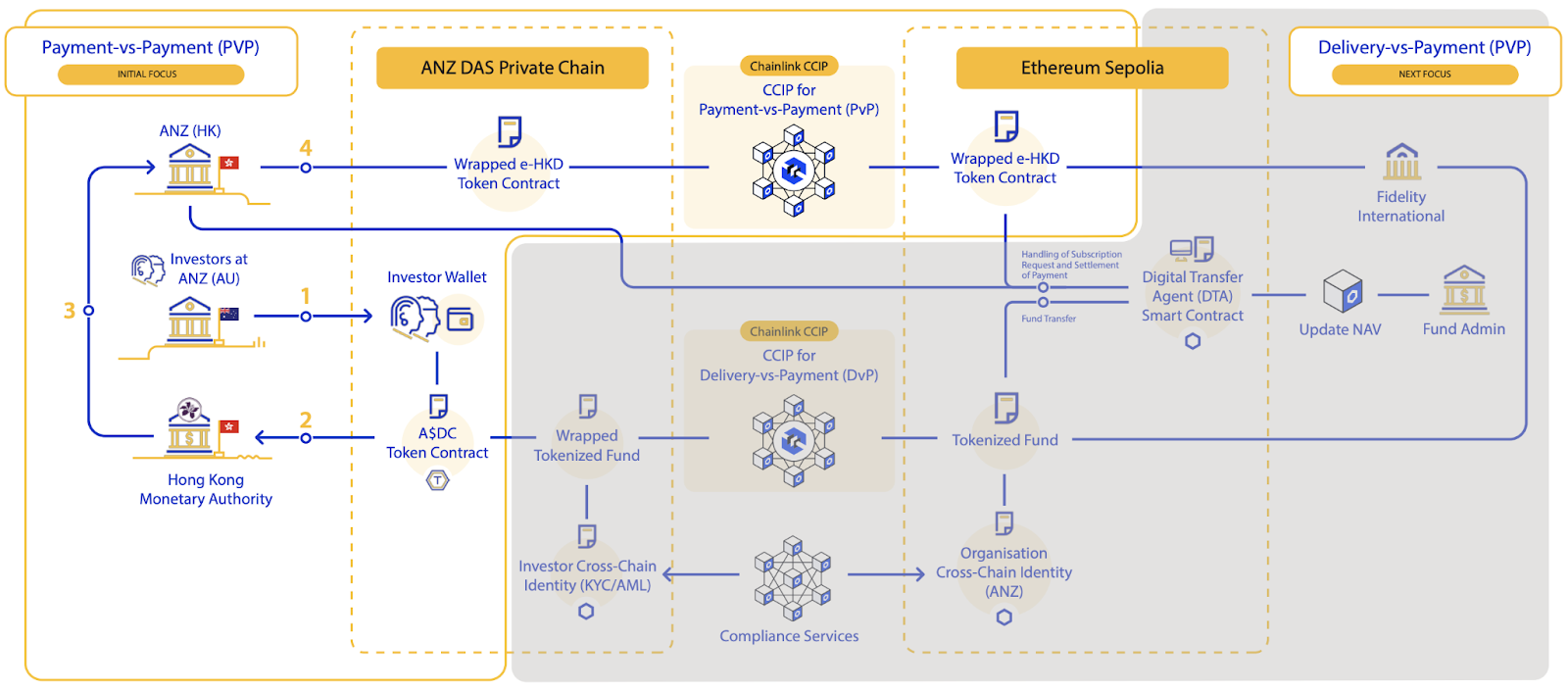

A recent initiative leveraging this architectural approach involved Visa, Fidelity International, ANZ bank, and Chainlink, under the Hong Kong Monetary Authority’s e-HKD+ program, where Chainlink infrastructure was used to verify investor eligibility, enable compliant cross-border settlement, and execute tokenized fund transactions across jurisdictions.

Bridging Traditional Financial Rails With Blockchain

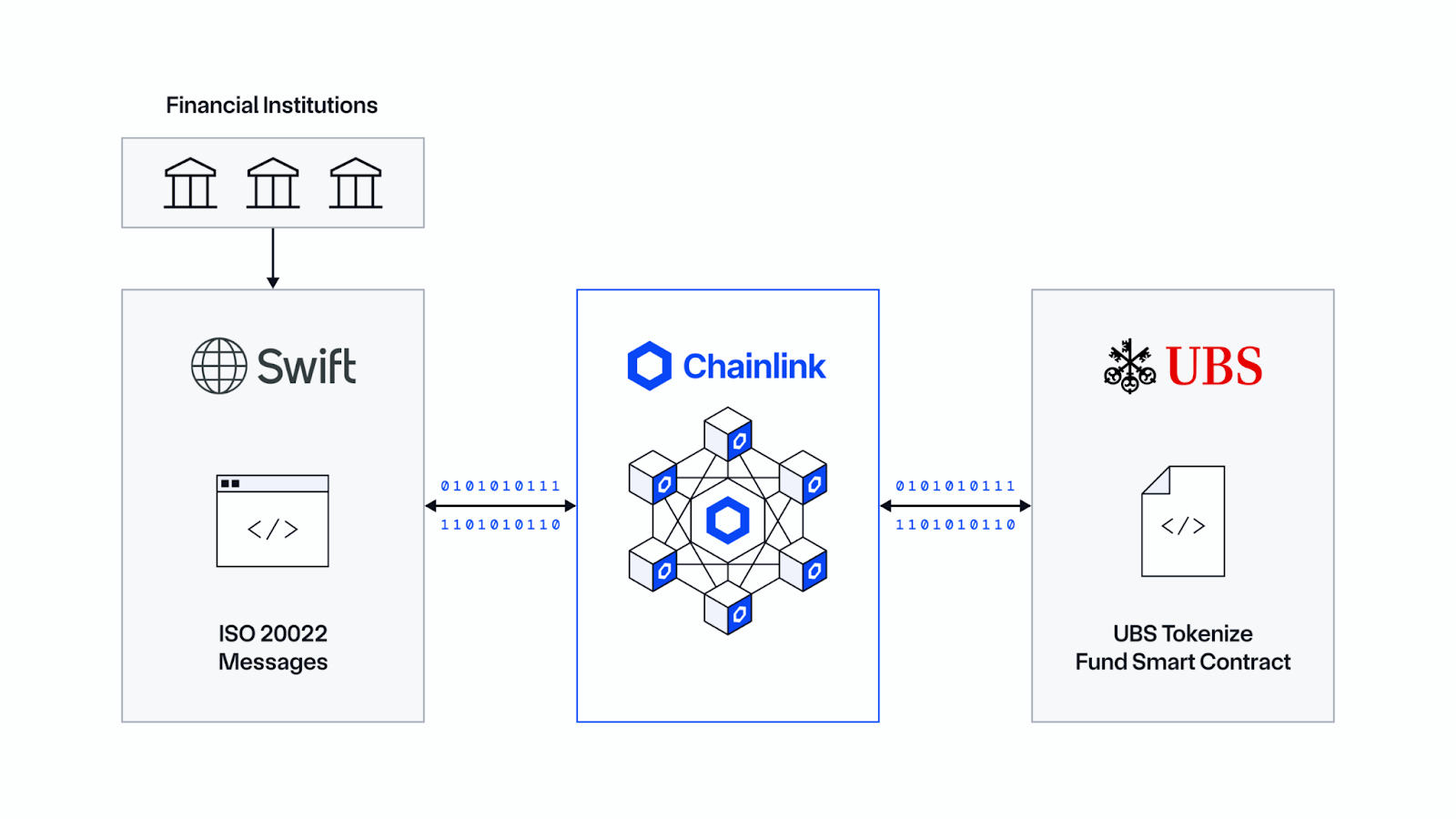

For tokenized funds to scale globally, they must integrate with the financial infrastructure institutions already rely on. The Chainlink Runtime Environment (CRE) enables financial institutions to initiate and manage onchain fund workflows directly from existing messaging standards and infrastructure, including Swift.

In collaboration with UBS, Chainlink demonstrated how subscription and redemption requests for tokenized funds could be initiated using ISO 20022 messages via Swift, with CRE orchestrating onchain execution through the Digital Transfer Agent (DTA) technical standard.

This model allows institutions to access blockchain-based fund infrastructure without replacing core systems, lowering adoption friction and accelerating institutional participation in tokenized fund markets.

Tokenized funds represent an evolution of traditional investment vehicles, not a departure from them. But realizing their full potential requires infrastructure that delivers the highest levels of security and reliability at an institutional scale.

Chainlink serves as this orchestration layer, enabling asset managers, administrators, custodians, and financial institutions to bring funds onchain while preserving the standards expected in global capital markets. By connecting blockchains with trusted data, cross-chain workflows, and existing financial systems, Chainlink enables tokenized fund models that are ready for real-world, institutional deployment.

As tokenization expands across public and private funds, Chainlink’s role as the connective tissue between onchain infrastructure and traditional finance will be central to how fund operations modernize.